Aani: The UAE's Sovereign Answer to Visa and Mastercard

12.5 million users. 774,000 merchants. Three-second settlement. Zero card fees. In under 30 months, Aani has gone from a Central Bank pilot to the backbone of UAE commerce — and a clear signal that the era of foreign payment rails in the Gulf is ending.

12.5 million users. 774,000 merchants. Three-second settlement. Zero card fees. In under 30 months, Aani has gone from a Central Bank pilot to the backbone of UAE commerce — and a clear signal that the era of foreign payment rails in the Gulf is ending.

The Big Idea

Paying someone in the UAE used to feel like a small task with surprising friction. You needed an IBAN. You waited a day for the transfer to arrive. If it was a merchant, the bank took a cut. If it was after-hours, the transfer waited for Monday.

Aani removed all of that.

Aani is the UAE’s national instant payment platform. It lets anyone — an individual, a shop, a business, a government office — send and receive money in under three seconds, any time of day, any day of the week, using just a mobile number or a QR code. No IBANs. No bank holidays. No waiting.

And it is not a private app competing for users. It is built, operated, and regulated by the Central Bank of the UAE (CBUAE) through its subsidiary, Al Etihad Payments. That one fact changes everything about how Aani fits into the economy.

|

12.5M+ Users |

774K Merchants |

3 sec Settlement |

6× YoY Growth |

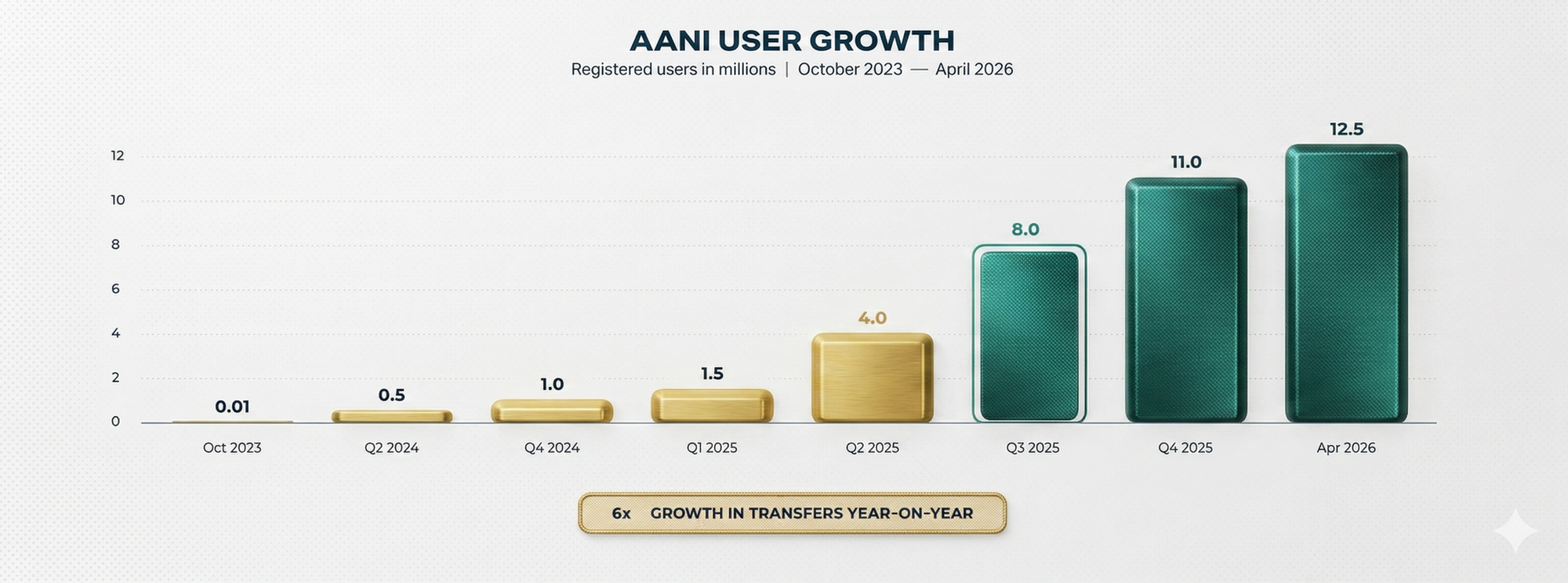

Figure 1 — How fast Aani grew: from pilot to 12.5 million users in under 30 months

The numbers tell a simple story. A platform that barely existed in 2024 is now used by more than one in two people in the country. That kind of growth curve only happens when something works better than what it replaces.

Why It Matters — The Business Story

To understand why Aani is more than just a convenience, think about what cash and cards actually cost the economy.

Cash is slow money. It has to be counted, transported, guarded, and deposited. Every step costs time and money. Businesses that rely on cash wait days to see their sales become usable capital.

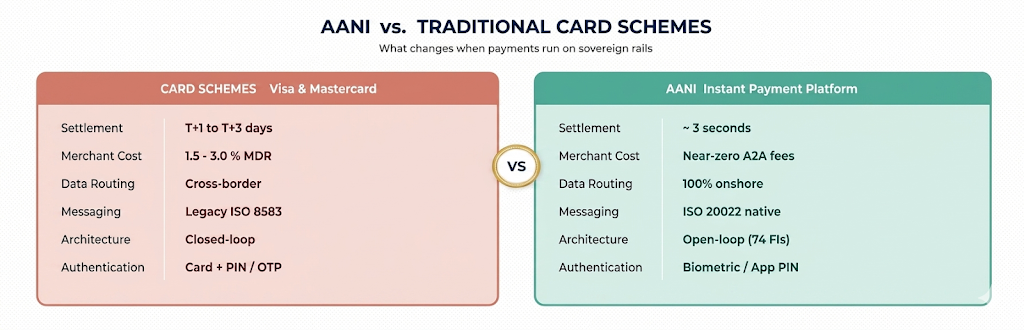

Cards are expensive money. Every swipe at a shop sends a small cut to Visa or Mastercard, another cut to the issuing bank, and another to the acquiring bank. For small merchants, that adds up to 1.5 to 3 percent of their revenue — money that leaves the UAE economy entirely.

Aani is fast, cheap, and sovereign. The money moves directly from one bank account to another in seconds, at near-zero cost to the merchant, and the data never leaves the UAE. That is the shift in one sentence.

Figure 2 — Side-by-side: what changes when payments move from cards to Aani rails

|

The insight: Dubai’s Cashless Strategy targets 90% digital

transactions by the end of 2026. That goal is not really about convenience —

it is about capturing the economics of domestic payments inside the UAE

instead of sending them abroad. Officials estimate the annual boost at more

than AED 8 billion. Aani is the rails that make the target reachable. |

Who Wins, and How

Different groups experience Aani differently. Here is what each one gets.

|

Shops

& Merchants Money arrives in seconds, not days. No more waiting for card

settlements or losing 2% of every sale. A small café that processes AED

50,000 a month in card payments can save roughly AED 12,000 a year just by

moving to Aani. |

Everyday

People Splitting a dinner bill, paying the babysitter, or sending

rent to a landlord no longer needs IBANs or bank branches. Just a mobile

number. Transfers up to AED 50,000 go through in seconds, for free, at any

hour. |

|

Banks

& Fintechs Banks lose some card-fee revenue but gain new lines of

business: request-to-pay, e-direct-debit, e-cheques, and B2B overlay

services. Fintechs get an open-loop platform they can build on top of —

something a private wallet could never offer. |

The

Government Clear visibility into money flows, less shadow economy, better

compliance, and tangible progress toward the cashless 2026 target. Wage

Protection System payments can now land instantly in workers’ accounts,

improving financial inclusion at the base. |

Aani Is Not Alone — It Is Part of a Bigger Plan

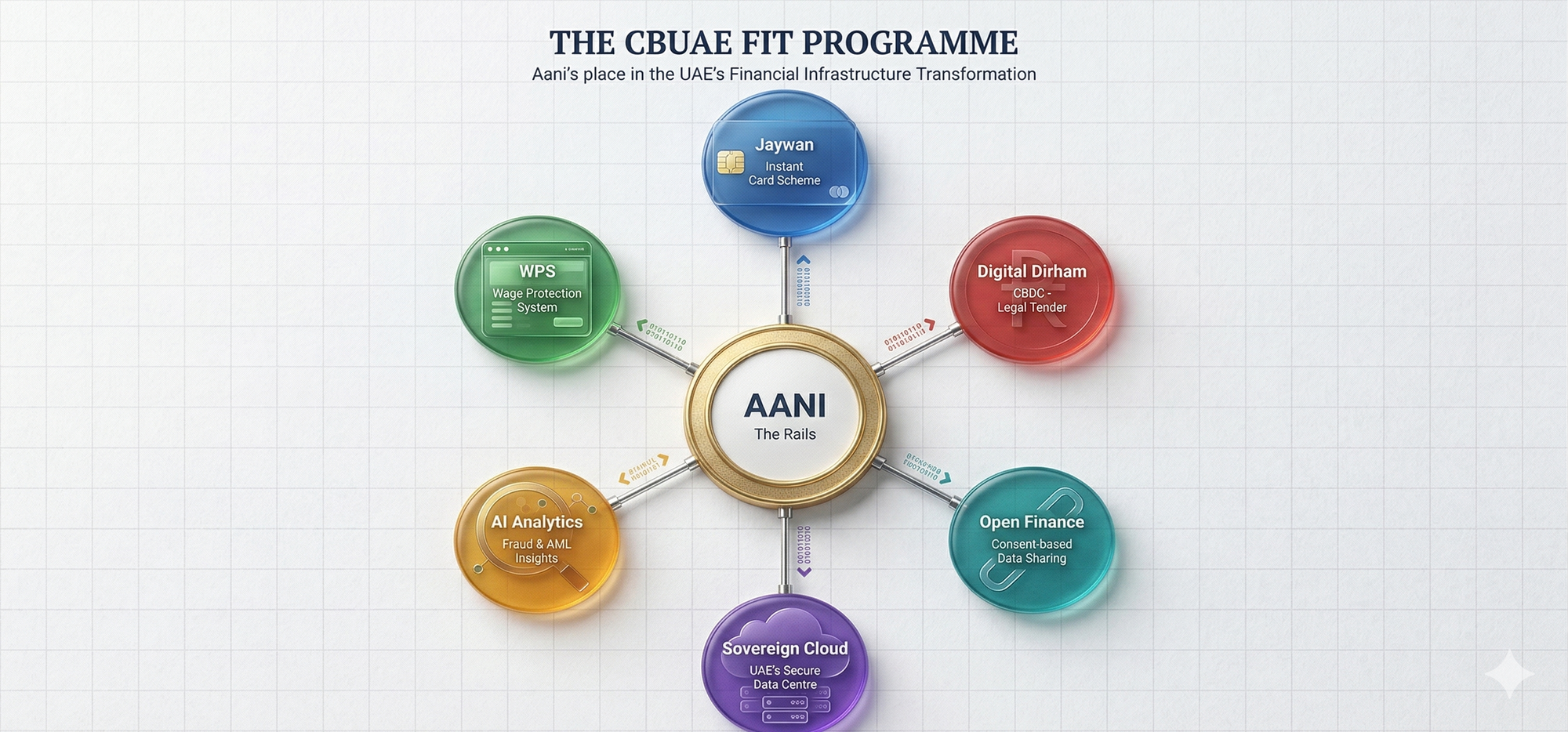

The Central Bank did not build Aani as a standalone product. It is one of several pieces in a larger blueprint called the Financial Infrastructure Transformation (FIT) Programme. Each piece does one job, and together they form a sovereign financial operating system for the country.

Figure 3 — Aani’s place in the CBUAE’s Financial Infrastructure Transformation Programme

Think of it as a system with six cooperating pieces:

Aani is the instant-transfer layer — the rails for moving money.

Jaywan is the national card scheme — the alternative to Visa and Mastercard for domestic card payments.

Digital Dirham is the central bank digital currency — official money in digital form, already legal tender.

Open Finance is the rulebook for sharing financial data safely with permission from the user.

Sovereign Cloud is the onshore data vault — built with Core42 — so no UAE financial data sits on foreign servers.

AI Analytics is the brain — a joint venture with Presight that watches everything for fraud, patterns, and insights.

The clever part is how these pieces connect. Aani moves the money, Jaywan handles domestic card swipes, the Digital Dirham introduces programmable money for the future, and Open Finance lets fintechs build new services on top of all of it — all running on the sovereign cloud, with AI watching for anomalies. No other country has put all six of these layers together under one regulator.

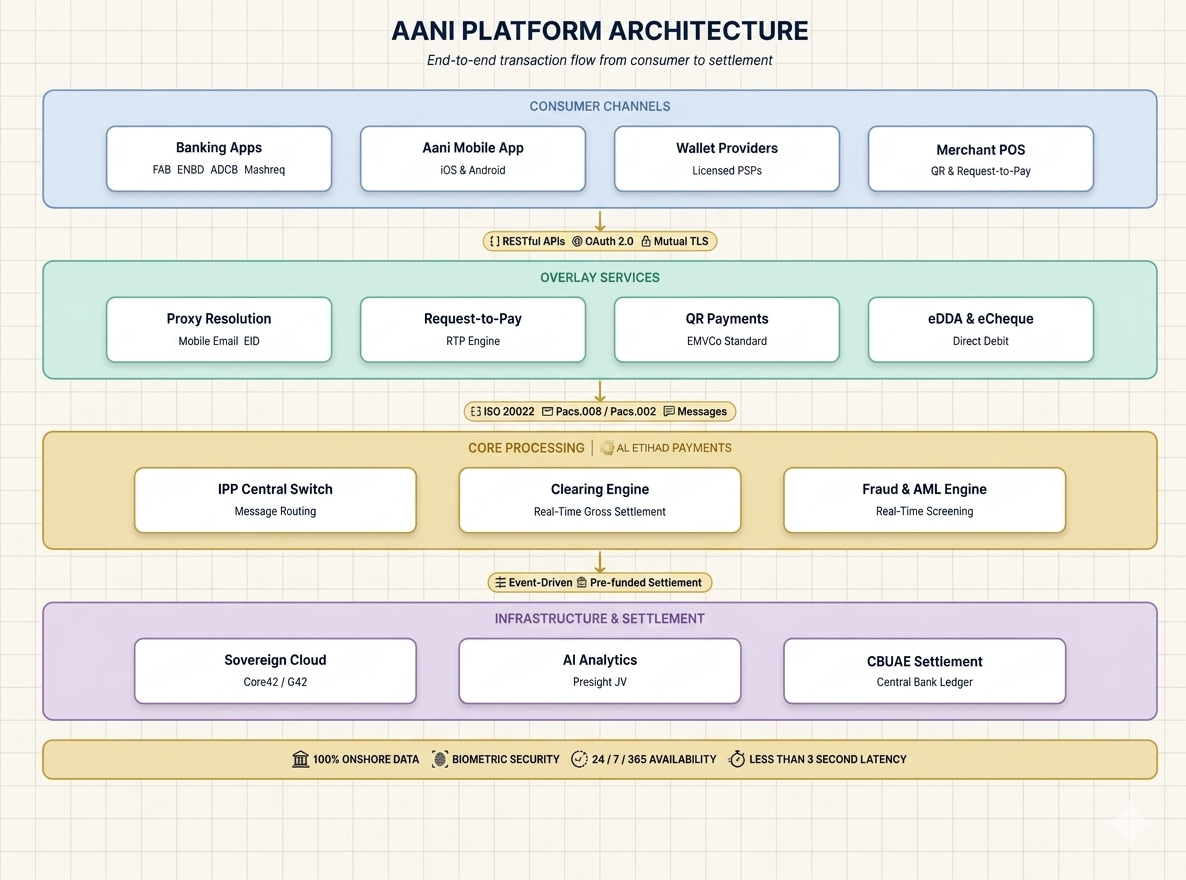

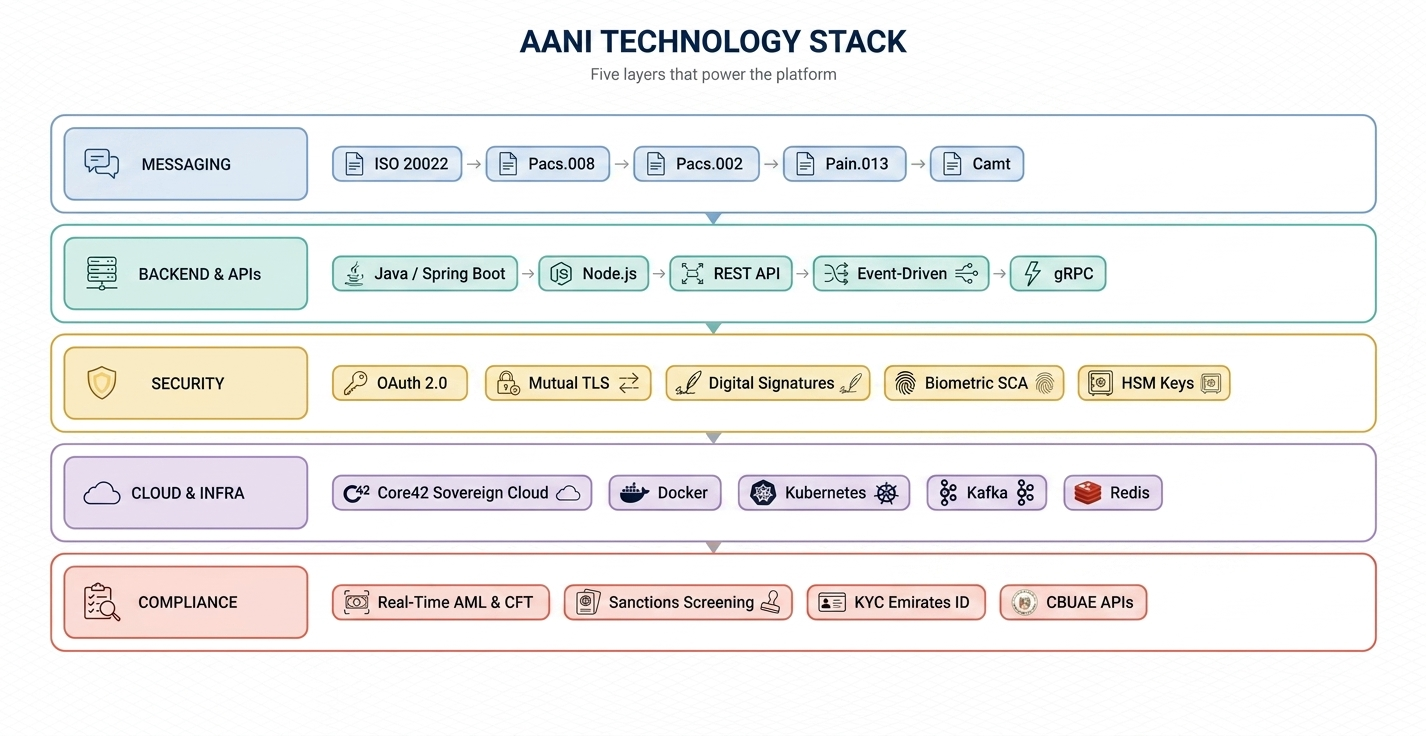

Under the Hood — How the Technology Actually Works

Most people do not care what happens after they tap “Send.” But for a banker, a developer, or a consultant, the technical design of Aani is where the real story lives. So here is the simple version.

Aani is built in four connected layers. Each layer has a clear job. Each layer talks to the next through a specific protocol. Nothing is accidental.

Figure 4 — The four layers of Aani and how they connect to each other

Reading the Architecture

Layer 1 — Consumer Channels. This is where you touch the system. Your banking app, the standalone Aani app, a licensed wallet, or a merchant QR code at the till. All of them connect to the rails through standard web APIs, protected by OAuth 2.0 and Mutual TLS — the same security layer your online banking already uses, but enforced at a national level.

Layer 2 — Overlay Services. This is where the smart features live. Proxy resolution is the trick that lets a mobile number map to an IBAN behind the scenes. Request-to-Pay lets a shop ask for payment instead of waiting. QR payments give merchants a cheap acceptance method. eDDA and eCheque handle recurring bills. You can think of this layer as the ‘apps’ running on top of the rails.

Layer 3 — Core Processing. This is the engine room, run by Al Etihad Payments. A central switch routes every transaction. A clearing engine settles each payment in real time on a gross basis — meaning there is no end-of-day batch, every transfer is final the moment it completes. A fraud and AML engine screens every movement instantly. The language spoken here is ISO 20022, the global standard that carries rich data with every message.

Layer 4 — Infrastructure & Settlement. The foundation. Everything runs on Core42’s sovereign cloud, so the data stays onshore. Presight’s AI watches every transaction. And the Central Bank’s settlement ledger is the final source of truth — the place where one bank’s reduction in balance becomes another bank’s increase.

Figure 5 — The five technology layers that power Aani — from messaging down to compliance

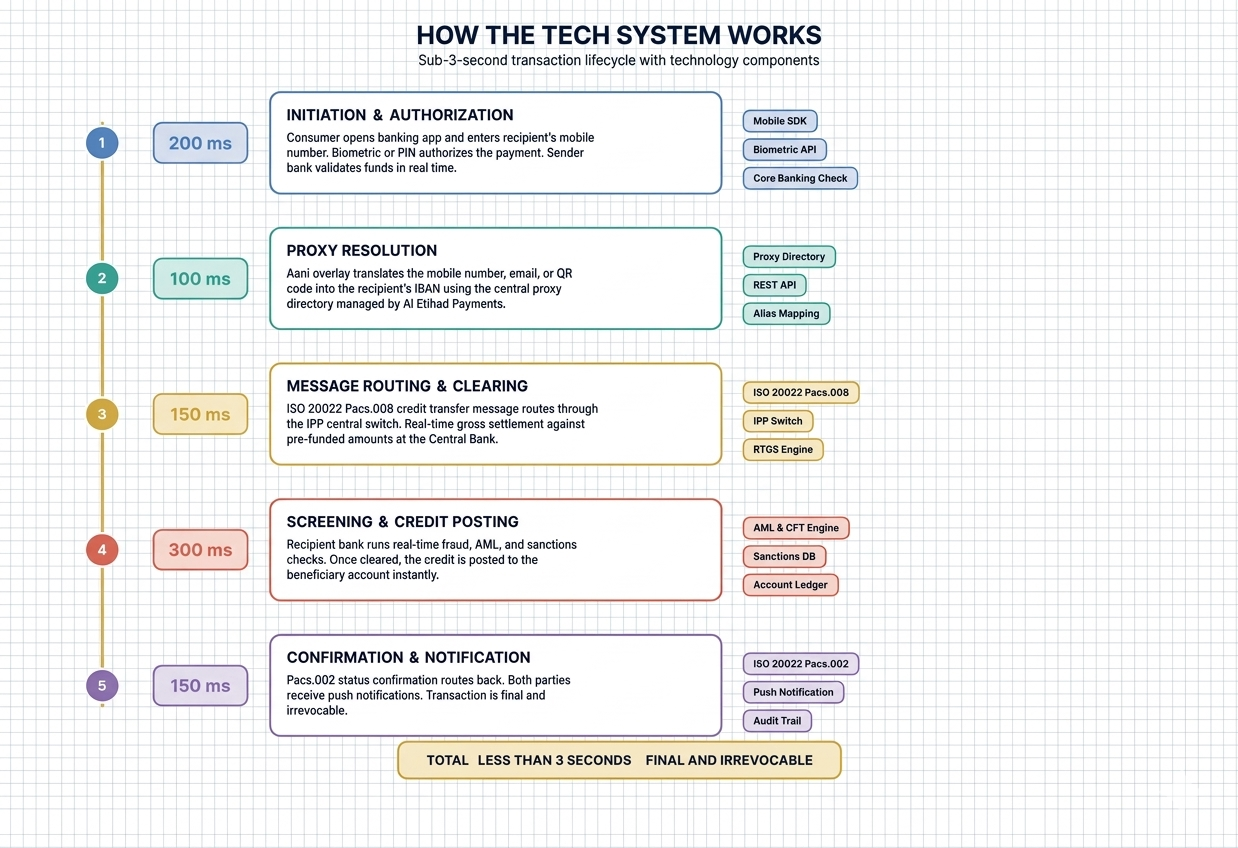

Following a Single Payment, Step by Step

Let us walk through what happens when you send your friend AED 100 over Aani. The whole thing takes under three seconds, but each of those seconds contains real work.

Figure 6 — The lifecycle of an Aani payment, with the technology behind each step

Step 1 — You tap Send. Your app asks for your fingerprint or PIN, and your bank checks in the background that you have the money. That check happens against the bank’s core banking system in under 200 milliseconds.

Step 2 — Aani finds your friend. You only typed a mobile number, but the money needs to land in an actual bank account. A central directory managed by Al Etihad Payments looks up which bank and account that mobile number belongs to. This is called proxy resolution, and it is the quiet trick that makes the whole user experience feel simple.

Step 3 — The message travels. Your bank packages the payment into an ISO 20022 message — specifically, a Pacs.008 credit transfer — and sends it through the central Aani switch. The switch routes it to your friend’s bank and triggers a real-time settlement against money your bank has pre-deposited at the Central Bank.

Step 4 — The receiving bank checks everything. Before the credit posts, the recipient’s bank runs the payment through its fraud, AML, and sanctions screening engines — all in real time. If everything is clear, the AED 100 hits your friend’s account.

Step 5 — Both of you get the notification. A Pacs.002 confirmation message routes back through the switch. Both phones light up. The transaction is final and cannot be reversed — there is no chargeback in Aani.

|

The technical insight: Every one of those steps is

stitched together by ISO 20022. It is the common language that lets the

consumer app, the overlay service, the central switch, the AML engine, and

the settlement ledger all understand the same message without translation.

That is what makes Aani feel instant. The speed is not magic — it is the

absence of friction between layers that used to speak different languages. |

How Aani Compares to the World

The UAE is not the first country to build an instant payment platform. India has UPI. Brazil has Pix. Singapore has PayNow. Each one is a success story in its own way. But Aani has one big advantage: it arrived late, which let the designers learn from everyone else’s mistakes.

|

Feature |

Aani (UAE) |

UPI (India) |

Pix (Brazil) |

PayNow (SG) |

|

Launch |

2023 |

2016 |

2020 |

2017 |

|

Messaging |

ISO 20022 |

Custom |

ISO 20022 |

ISO 20022 |

|

Settlement |

Real-time

gross |

Deferred |

Real-time

gross |

Deferred |

|

Sovereign

Cloud |

Yes (Core42) |

No |

No |

No |

|

CBDC link |

Digital

Dirham |

e-Rupee pilot |

Drex pilot |

No |

|

Open Finance |

Built-in |

Separate |

Separate |

Planned |

Aani is the only instant payment platform in the world that was designed from day one to connect with a national CBDC, an open finance framework, and a sovereign cloud — all under the same regulator. That is not a small distinction.

The Economic Picture

Zoom out and Aani becomes more than a payment tool. It becomes a way to make the whole UAE economy move faster.

Money moves faster. When a shopkeeper receives payment instantly instead of waiting two days, that same cash can buy new inventory the same afternoon. Multiply that by hundreds of thousands of businesses and the economy speeds up, quietly but measurably.

Less shadow economy. Digital transactions leave a trail. That makes tax collection cleaner, AML enforcement stronger, and regulatory oversight more accurate — without anyone having to be watched by a person.

More people in the formal system. A construction worker paid through the Wage Protection System can now use Aani directly from his salary card to send money home or pay rent. He no longer needs a branch, a remittance desk, or a plastic card. That is financial inclusion built into the rails.

The Takeaway

Aani looks like a simple app when you use it. But underneath, it is a careful piece of national infrastructure — cheaper than cards, faster than bank transfers, safer than cash, and designed to keep the economics of UAE commerce inside the UAE.

For banks, it is a shift in revenue model from interchange to overlay services. For merchants, it is a break from paying a tax to global card schemes. For consumers, it is just the new normal. For the regulator, it is the rails that make the 90% cashless target look achievable rather than ambitious.

The rails are already live. The question now is not whether the UAE economy will become mostly digital — it will. The question is how quickly the banks, finTechs, merchants, and trainers of the region adapt to a world where sovereign rails are the default. The ones who move first will define the next decade of UAE finance.